Canada Caregiver Credit Basics

Before embarking on the mechanics of the credit itself, we must understand some definitions that affect the credit.

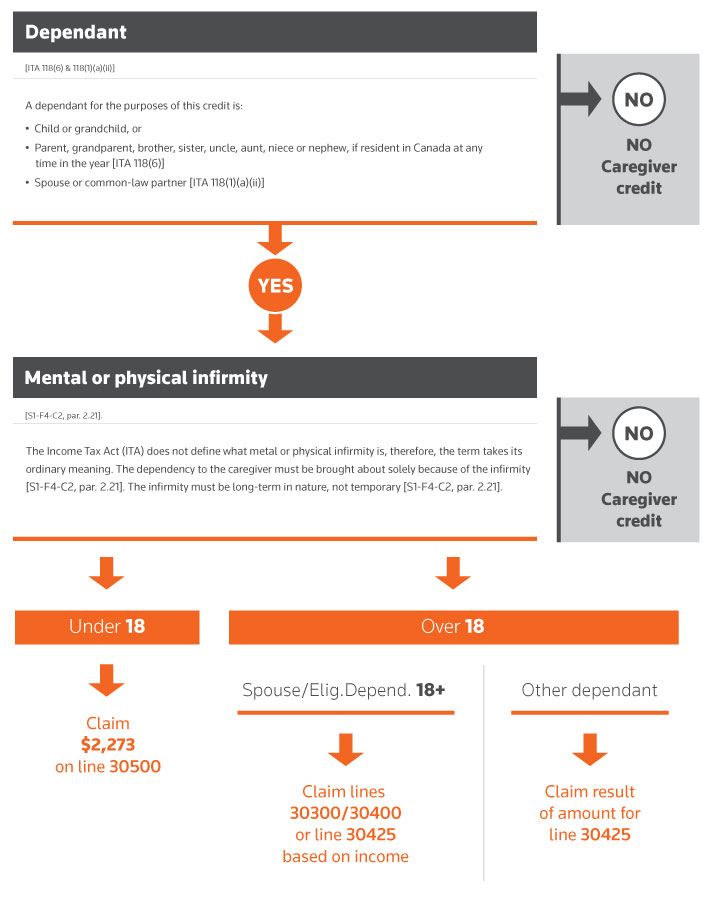

Mental or physical infirmity

The Income Tax Act (ITA) does not define what mental or physical infirmity is. Therefore, the term takes its ordinary meaning. The dependency to the caregiver must be brought about solely because of the infirmity [S1-F4-C2, par. 2.21]. The infirmity must be long-term in nature, not temporary [S1-F4-C2, par. 2.21].

Dependant

A dependant for the purposes of this credit is:

- child or grandchild [ITA 118(6)],

- parent, grandparent, brother, sister, uncle, aunt, niece or nephew, if a resident in Canada at any time in the year [ITA 118(6)], or

- spouse or common-law partner [ITA 118(1)(a)(ii)].

The Mechanics of the Credit

The credit can be broken down to two broad categories:

- Dependants under the age of 18 [ITA 118(1)(b.1)]

- Dependants aged 18 and over [ITA 118(1)(a)(ii) & 118(1)(b)(ii) & 118(1)(d)]

Dependants under the age 18 [ITA 118(1)(b.1)]

For dependants under the age of 18, the Canada Caregiver Credit is summed up in one claim on the tax return, a non-refundable tax credit of $2,273 (in 2020) per eligible child on line 30500 of the T1. To be eligible for this credit for dependants under 18, the dependant (see above) must be:

- under the age of 18 at the end of the tax year; and

- by reason of mental or physical infirmity (see above), is likely to be, for a long and continuous period of indefinite duration, dependent on others for significantly more assistance in attending to the child’s personal needs and care, when compared to children of the same age.

Dependants aged 18 and over [ITA 118(1)(a)(ii) & 118(1)(b)(ii) & 118(1)(d)]

The eligibility requirements are the same as with dependants under 18, that is, the person is dependent on the individual because of a mental or physical infirmity.

For this category, you must subdivide the dependants into two sub-categories:

- Spouse/common-law partner and eligible dependant aged 18 and over [ITA 118(1)(a)(ii) & 118(1)(b)(ii)]

- Other dependants [ITA 118(1)(d)]

For spouses and eligible dependants aged 18 and over, the caregiver credit is an additional amount of $2,273 (in 2020) added to the existing spousal amount credit (line 30300 of the T1) and eligible dependant amount (line 30400 of the T1). Based on the income gained, spouses/eligible dependants can be claimed simultaneously between the lines mentioned above and Canada Caregiver Amount on line 30450.

Other dependants (see dependant definition above) are claimed specifically on the Canada Caregiver Amount line 30450.

The infographic included in this article will show in detail what gets claimed for each type of dependant.

Quebec Natural Caregiver Credit

The Quebec natural caregiver credit is a refundable credit claimed for dependants being cared for by caregivers. The credit itself is split into two components:

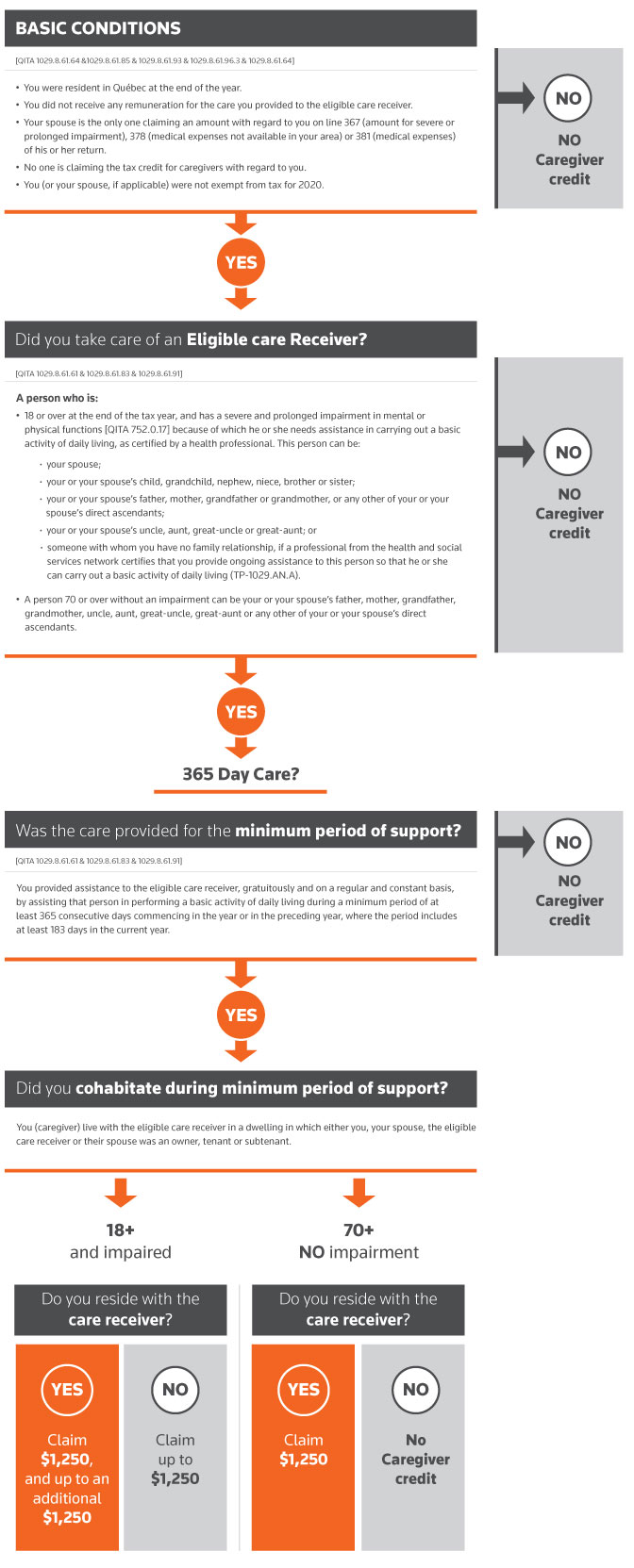

- Dependant aged 18 or over who has a severe and prolonged impairment and needs assistance in carrying out a basic activity of daily living [QTA 1029.8.61.64 &1029.8.61.85 & 1029.8.61.93 & 1029.8.61.96.3]

- Dependant 70 and over without an impairment [QTA 1029.8.61.64]

Before getting into the components, it’s important to understand to the definition of the dependant or, as designated by Revenu Québec, the eligible care receiver.

An eligible care receiver [QTA 1029.8.61.61 & 1029.8.61.83 & 1029.8.61.91] is a person who is:

- 18 or over at the end of the tax year, and has a severe and prolonged impairment in mental or physical functions [QTA 752.0.17] because of which he or she needs assistance in carrying out a basic activity of daily living, as certified by a health professional. This person can be:

o your spouse;

o your or your spouse’s child, grandchild, nephew, niece, brother or sister;

o your or your spouse’s father, mother, grandfather or grandmother, or any other of your or your spouse’s direct ascendants;

o your or your spouse’s uncle, aunt, great-uncle or great-aunt; or

o someone with whom you have no family relationship, if a professional from the health and social services network certifies that you provide ongoing assistance to this person so that he or she can carry out a basic activity of daily living (TP-1029.AN.A).

- A person 70 or over without an impairment can be your or your spouse’s father, mother, grandfather, grandmother, uncle, aunt, great-uncle, great-aunt or any other of your or your spouse’s direct ascendants.

Dependant aged 18 or over who has a severe and prolonged impairment [QTA 1029.8.61.64 &1029.8.61.85 & 1029.8.61.93 & 1029.8.61.96.3]

For this component, the caregiver can claim the credit regardless of whether they live with the eligible care receiver or not. The difference is in the maximum amount that can be claimed. If the caregiver lives in a dwelling in which either they, their spouse, the eligible care receiver or their spouse was an owner, tenant or subtenant, then the claim is $1,250 (2020), and an additional amount for $1,250 which gets reduced based on income. If you do not live with the care receiver, the maximum amount you can claim is an additional amount for $1,250 which gets reduced based on income.

In either case, the caregiver must provide care for 365 consecutive days, including at least 183 in the current taxation year.

Dependant 70 and over without an impairment [QTA 1029.8.61.64]

For these eligible care receivers (see definition above), the caregiver must live with the dependant for 365 consecutive days, including at least 183 in the current taxation year. The claim for this component is $1,250.